Where Asia’s $103 Billion Game Market Is Actually Growing

Jen Donahoe's five takeaways from Niko Partners’ 2026 Market Model.

If you listen to our podcast, This Week in Games, you know we spend most of our time on the Western market, usually tier one countries and most often the US. We do that for a good reason, because the US is the biggest single revenue opportunity in the West. What we say less often is that more than half of all gaming revenue comes from the East, and that is the part of the map we tend to skip. Partly because the key Asian markets are extremely difficult for Western publishers to penetrate due to legal (China) and/or cultural (Korea, Japan) constraints.

Niko Partners are the experts in this region, and their data genuinely helps us understand the trends and the growth opportunities across both revenue and players. For a Western studio, that data earns a place in your strategy only when you have a specific growth target and a game built to meet what Eastern audiences actually want. For most of us, that is not where we sit, but we can always learn from the trends of what is working and what is not in Eastern markets. Also, because what works in the key Asian markets today, tends to be what works in Western markets in two to four years later.

Here are the five takeaways that matter, and what they mean for those of us in the West.

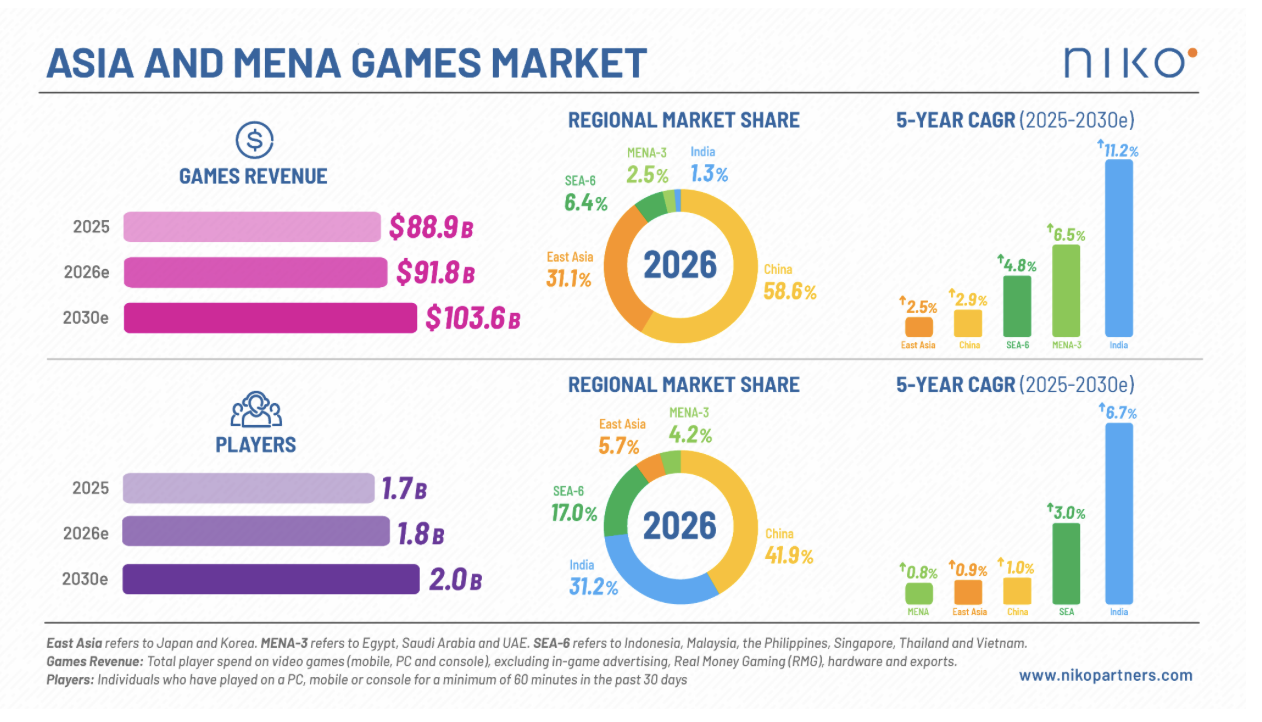

Niko Partners’ 2026 Market Model tracks 13 markets across Asia and MENA, which together made $88.9 billion in 2025 and should reach $103.6 billion by 2030, a 3.1% compound annual growth rate, with the player base climbing toward 2 billion. Those 13 markets are roughly 46.3% of global game revenue, so this is close to half the industry. The headline number is real. Where it gets interesting is which part of that market is actually growing.

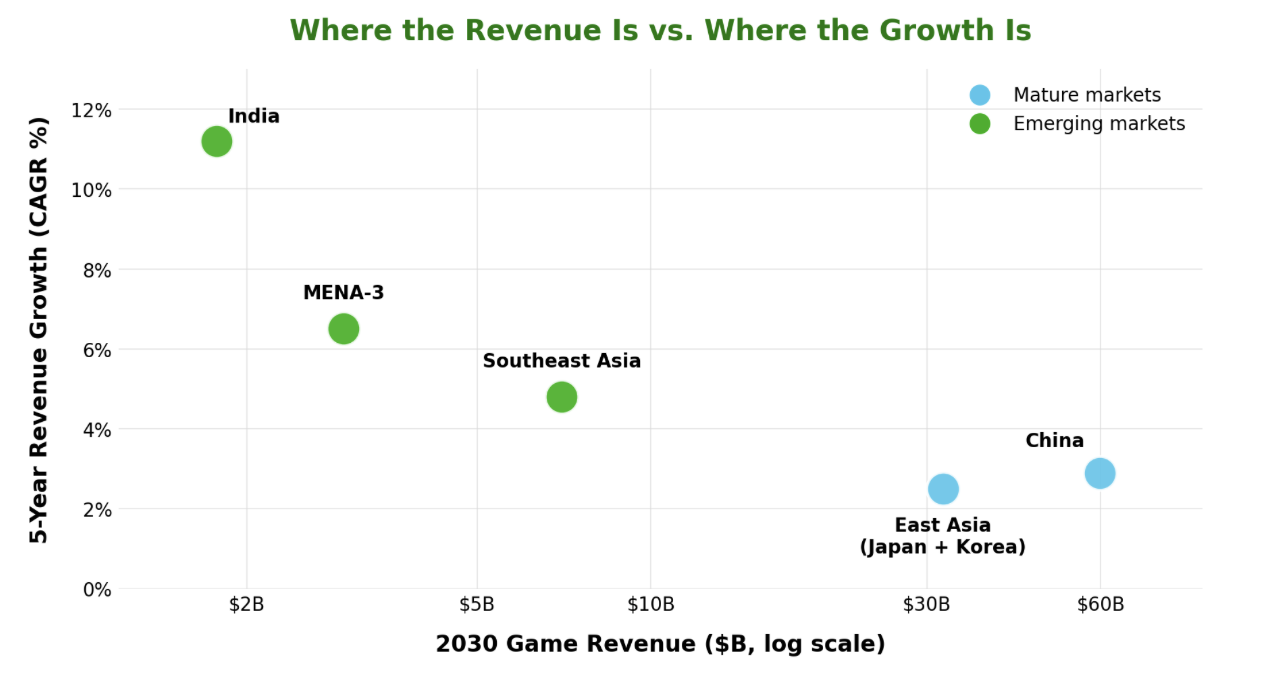

1. Three mature markets hold 88.6% of the revenue and almost none of the growth.

In terms of revenue, Asian markets are Japan, Korea and China with Singapore, KSA, UAE, India and Taiwan filling the gaps.

Niko’s numbers show China, Japan, and Korea holding 88.6% of regional revenue in 2030 while growing slowly, China at 2.9% a year and East Asia at 2.5%. The fast growth rates belong to India at 11.2%, MENA-3 at 6.5%, and Southeast Asia at 4.8%, all off small bases.

The piece people miss is the gap between players and dollars. India adds close to 200 million players this cycle while its revenue only climbs from about $1 billion to $1.8 billion, which works out to roughly $2 a player against $371 a player in Korea.

My read: the growth you keep hearing about in these markets is player growth, and that is a very different thing from revenue growth. For most Western studios the money is still in the mature markets, and even those are a hard door to walk through, because China, Japan, and Korea are concentrated markets where local titles win and foreign entry is the exception.

The emerging markets are worth entering only with a late life cycle game and the local expertise to capture the thin revenue that exists.

The mature markets hold the revenue while the emerging markets hold the growth. Revenue on a log scale. Source: Niko Partners 2026 Market Model.

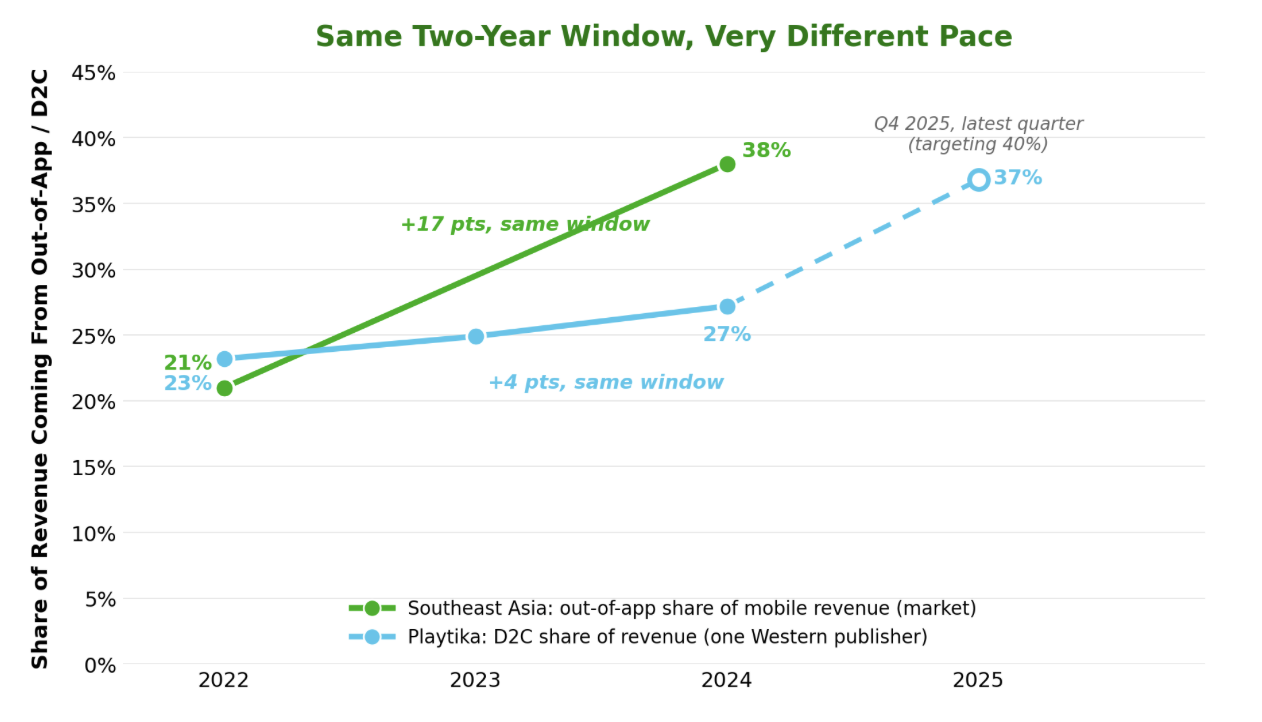

2. A third of players now prefer to pay outside the app.

This is the number I had not seen before. Niko’s 2026 model finds more than 30% of players across the 13 markets now prefer to transact outside the game itself, and as far as I can tell there is no public baseline for it yet, which makes it close to a proprietary read on player behavior.

On the revenue side, where data does exist, the shift is just as clear. Niko’s own work shows out of app revenue in Southeast Asia jumped from 21% to 38% of mobile revenue between 2022 and 2024. Playtika, a Western publisher, moved its direct to consumer share from 23% to 27% over the same two years, then accelerated to 37% by late 2025 and is now targeting 40%.

My read: the out of app shift is real, it is already showing up in public company financials, and Asia is about two years ahead of the West and still pulling away. For us that means building direct to consumer now rather than later, because the players have already decided they prefer it and the operators who move early keep the margin the platforms are losing.

Out of app revenue share over the same 2022 to 2024 window, full year to full year, with Playtika’s 2025 quarter shown as the dashed catch up. Sources: Niko Partners and Coda, and Playtika investor reports.

3. PC, console, and mini games are where the new growth is.

Let me concede the obvious first. The revenue here is still driven by a handful of very big mobile games that keep printing. What is interesting is where the new segments are opening up. Japan’s PC market is growing 8% this year, mini games (lightweight, instant play titles that run inside super apps like WeChat and Douyin with no separate download) are now nearly 20% of mobile spend in China, and Switch 2 is selling well. The genres pulling that growth are specific. In India, players are moving into casual and other non battle royale games after years of battle royale dominance, and in China the boutique segments doing well include dating simulation, social deduction, realistic sports, and idle RPGs.

My read: not every team is swinging for a grand slam, and some are looking for singles, doubles, and triples. These emerging segments are where a smaller studio can place a bet without betting the company, and which one fits depends on your own strengths, with mini games and HTML5 pulling at some teams and PC pulling at smaller indies.

4. Two shifts are widening the player base: more women, and more players in new markets.

Women crossed 40% of players for the first time and now make up 42%, with the steepest gains in India and the MENA-3 markets that ran 80% male only five years ago. Separately, the fastest growth in raw player numbers is coming from India, Indonesia, and Vietnam, with Indonesia heading toward 144 million players and Vietnam toward 68 million by 2030.

My read: the next players entering this market look nothing like the ones most games were designed for. If you do build for the East, the audience, the art, the UA creative, and the live ops all have to reflect a broader and more diverse base than the assumptions baked into a typical Western title.

5. Players see GenAI very differently in the East than in the West.

This is where the Niko data is genuinely useful for us. Player sentiment toward generative AI is materially more positive in Asia than in Western markets, most Asia based studios already use the technology, and they report real development efficiencies from it. The acceptance has limits even there, since players back AI inside development workflows and push back when it touches core art or marketing.

My read: the East versus West perception gap is the takeaway for us, not the adoption rate. Western players are more negative, so the safe place to lean on GenAI is the backend and the development pipeline, where it lowers cost without touching the player. In player facing marketing, comms, and PR, the same tools invite blatant negativity here that they would not draw in the East, so that is where we should tread carefully.

The bottom line

This is why we keep an eye on the East even though we spend our time in the West. The growth is real and worth watching, but it has moved to the emerging markets and a broadening player base while the money stays in China, Japan, and Korea. For most of us that makes Niko’s data a map to learn from rather than a market to chase.

Two trends do cross over and are worth acting on now, building your direct to consumer muscle ahead of the curve and being deliberate about where you put GenAI, and a smaller team hunting for a single or a double can find one in the new segments.

Currency swings, rising memory prices, and the 2026 Iran conflict all press on spending in the near term, and even so the region outgrows the global average through 2030. So watch the East and learn from it, and act on it only where it actually touches your game.