The Founder’s Dilemma: Equity vs. User Acquisition Financing

By Michail Katkoff, who enjoys telling finance folks that EBITDA wasn’t made for games.

For most founders, scaling a successful game comes with a painful trade-off: raise more equity to fuel growth and give away a permanent slice of the company, or slow down and watch competitors catch up.

UA financing breaks that stalemate. It lets you scale proven titles, launch new ones, and expand your portfolio without handing over more of your cap table.

But UA financing is not the solution for every game or company. This write-up explores when and how to use this powerful lever.

—

Finance and marketing folks like to throw lots of acronyms, and I don’t want this write-up to be only read by those with an MBA.

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. It measures a business's profitability from its regular operations, without considering expenses.

CapEx means Capital Expenditures. It refers to the investments a company makes to acquire, improve, or maintain long-term assets such as buildings, land, machinery, or equipment.

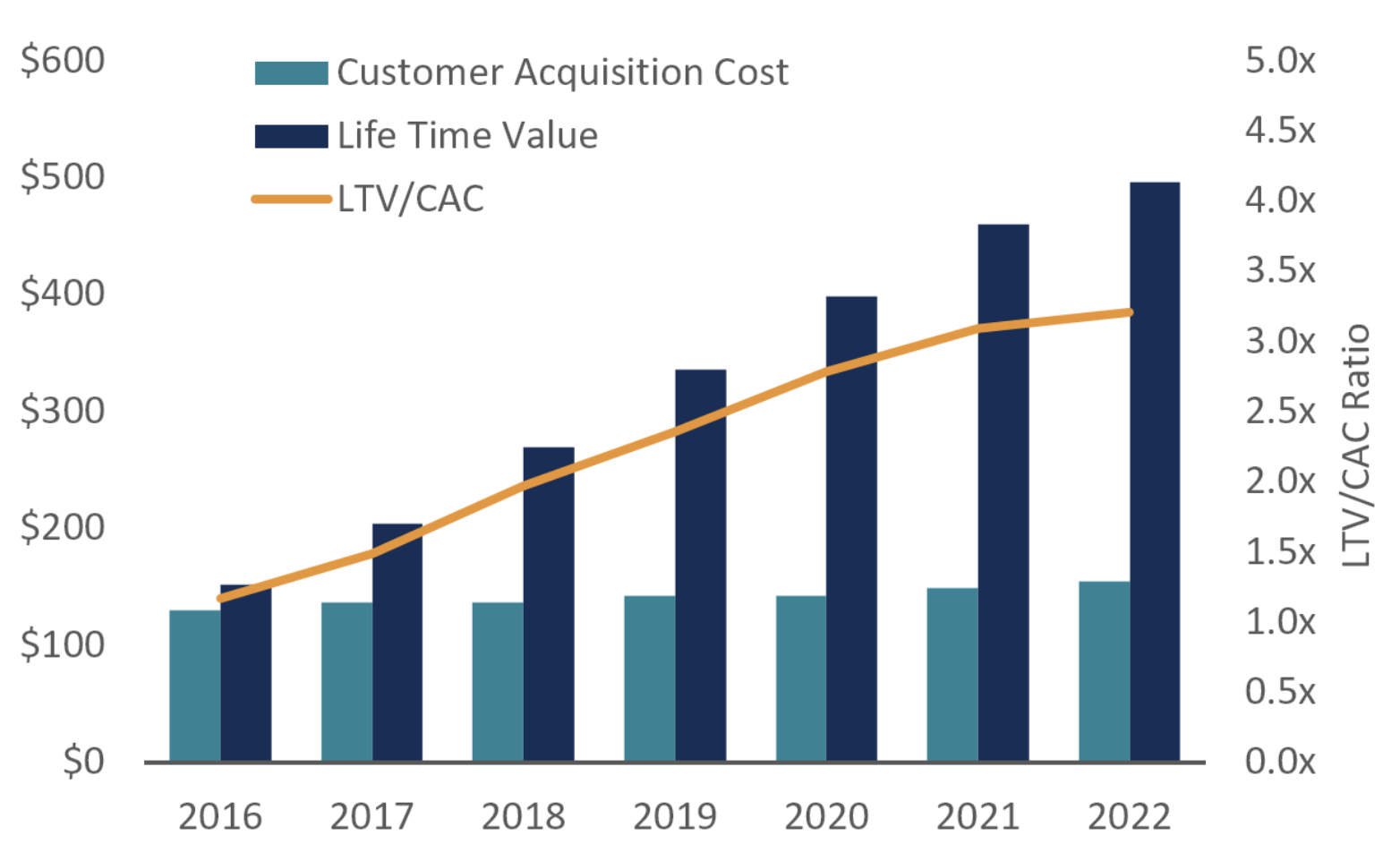

LTV stands for Life-Time Value. This is essentially a measurement for user value and sets the ceiling for CAC, which is the customer acquisition cost.

The LTV curve represents the growth of user value over time. For example, an LTV curve for Netflix is linear as users spend roughly the same amount every month for years. In a simple game, it can go up fast and plateau as users spend in the beginning and churn.

A cohort is a group of users coming. In this context, by cohort, I refer to a user group that joined in a specific month and tracks their performance. Such as the performance of the January cohort versus the June cohort.

The Problem With EBITDA Thinking

Every late-stage gaming or app founder has felt it: the numbers look good, the LTV curve is smooth, UA is performing… and yet your CFO says the growth budget is frozen because EBITDA is trending the wrong way. That’s not a business problem; that’s an accounting problem.

EBITDA wasn’t designed for companies like ours. It was born in the 1980s when cable operators were digging trenches and laying miles of wire. The cable companies needed a way to show investors the real earnings power of these companies, which were all spending heavily on CapEx and taking huge depreciation hits. Their fix was to add back depreciation and amortization, creating EBITDA, a metric meant to strip away accounting noise from capital-intensive growth.

Fast forward to 2025: gaming, SaaS, and consumer apps are not CapEx-heavy. Our “factory” is user acquisition spend. But unlike cable companies, we expense our “CapEx” immediately. The $1M you spend on UA this month might return $3M in gross profit over the next 24 months, but on paper, your P&L (profit and loss statement) just took a $1M hit. So companies fixate on a short-term EBITDA target and cut UA, even if the ROI is fantastic.

As Pranav Singhvi, Managing Director of General Catalyst, puts it on the Deconstructor of Fun podcast below, “EBITDA is anti-growth. Quite literally, if you spend more on UA, your EBITDA will go down. Why would you create a covenant that’s anti-growth?”

The right mental model here is EBITCAC, EBITDA plus Customer Acquisition Cost. By adding back your discretionary UA spend, you reveal the true profitability of your existing customer base.

If EBITCAC is positive, you’re fundamentally profitable. You could shut off UA tomorrow and generate cash. The fact that you’re “negative” on EBITDA is just proof that you’re investing in future growth.

What UA Financing Really Is and When It Makes Sense

UA financing exists to solve a single bottleneck: the balance sheet constraint. Even if your LT-to-CAC ratio is beautiful, you can only scale spend as far as your cash position allows. Push past it, and you’ll run out of money before your cohorts pay back.

Example: LTV/CAC ratio above 3.0 is often considered good, but what’s ‘good’ depends on the business model and context.

In the old economy, manufacturers solved this with asset-backed loans against physical factories. In gaming, our “asset” is the predictable cash flow from high-LTV cohorts, but until recently, capital markets didn’t know how to underwrite it.

That’s where UA financing comes in. At its core, it’s specialized growth capital that funds a defined portion of your UA spend, often 50–80%, and gets repaid only from the revenue of the cohorts acquired with that money. If the cohorts underperform, the financier takes the hit, not you. If they perform, you pay an agreed multiple on their initial investment, then keep 100% of the upside thereafter.

Crucially, the payback schedule is matched to the cohorts’ revenue curve, eliminating the asset-liability mismatch that makes traditional debt risky for growth.

Joe Wadakethalakal, CEO and co-founder of PvX Partners, describes the impact bluntly: “Your job is to make as many net new dollars as you can, as fast as you can, with as little risk as possible. UA financing, when your cohorts are proven, is the cheapest and fastest way to do that.”

But UA financing is not a fit for everyone.

Joe’s PVX Partners looks for companies already spending a few hundred thousand dollars a month on UA, with 9–12 months of data at that level, and LTV curves that keep rising months after acquisition. Pranav’s Customer Value Fund, on the other hand, targets scale-ups spending $2M+ per month with predictable unit economics. In both cases, the product must be ready, no fundamental design overhauls every sprint, and the UA machine must be proven enough that new capital can accelerate it rather than fund experiments.

Used in the right window, UA financing lets you stretch paybacks from the “safe” 12–15 months to 24–36 months if your LTV supports it. As Pranav says: “If the lifetime value supports it, shouldn’t the payback be an output of the marginal CAC equals marginal LTV equation, not an arbitrary 12-month target?”

That’s how companies like Superplay scaled into billion-dollar outcomes without raising hundreds of millions in equity. UA financing is not a replacement for VC; it’s a complement, freeing equity dollars for product bets while the UA machine gets its dedicated fuel source.

Philosophical Musing

Beneath all the talk about metrics and financing structures is a much simpler truth: the CEO’s real job is raising capital and allocating it in the most effective way.

Ultimately, the CEO's job is not shipping features, optimizing monetization, doing industry talks, or building culture decks; it’s deciding where every incremental dollar goes and at what cost of capital.

If you want to maximize long-term free cash flow per share, you have to fund growth without giving away even an increasing share of your company after you just found the elusive product market fit and are finally scaling. The fact is that the cheapest dollar available isn’t equity.

Equity is for unstructured risk. Creating new games, entering new geos, experimenting with no history. UA financing is for the predictable, measurable machine that turns $1 into $3. Get that alignment right, and you can capture market share now, when your LTV advantage is real, before competitors close the gap. Miss it, and you’ll either stall growth or dilute yourself out of the upside.

Gaming is a zero-sum market. As Joe puts it: “In gaming, these windows of opportunity to capture excess LTV don’t come often. You might have three to six months before the gap closes. That’s when you push hard, grab market share, and make it expensive for others to catch up.”

UA financing won’t create growth for you, but it can give you the balance sheet power to make it happen.