Fair Weather Founders, Dead Equity, and the Cliff that Saves

Written by Phylicia Koh, General Partner at Play Ventures, a leading early-stage gaming VC fund. Phylicia has led investments into Alter (an avatar tech company acquired by Google) and gaming startups at all stages. Prologue written by Mishka Katkoff, who benefited personally from the 2-year cliff.

We had to part ways with two co-founders during the first two years after starting our company. No departure of a founder is easy. You always imagine going all the way or until the bitter end with the people you start the company with.

For most startups, losing two co-founders would have been a death blow in the investors' eyes. But in our case, we avoided the disaster. By disaster, I don’t mean a potential talent gap that a leaver might have left. The real disaster occurs when the exiting co-founder takes their vested shares with them and turns them into dead equity.

In our case, we were protected by our 2-year vesting cliff agreement that our investor, Play Ventures, strongly recommended. In other words, we as founders didn’t receive any of our vested shares until 2 years had passed.

This simple contract, which we didn’t like at first, ended up saving our startup.

Don't just take my word for it, take Phyllicia’s word. She has the data and founders from Play’s network tell their stories.

*Founder breakups are sensitive. Names have been changed to protect the founders' identities, companies, and to be compliant with non-disclosure agreements.

The Hard Truth About Startup Timelines

Over 60% of successful startups pivot at least once before finding product-market fit. Yet we're still clinging to vesting terms created for a world where companies found their stride in months, not years.

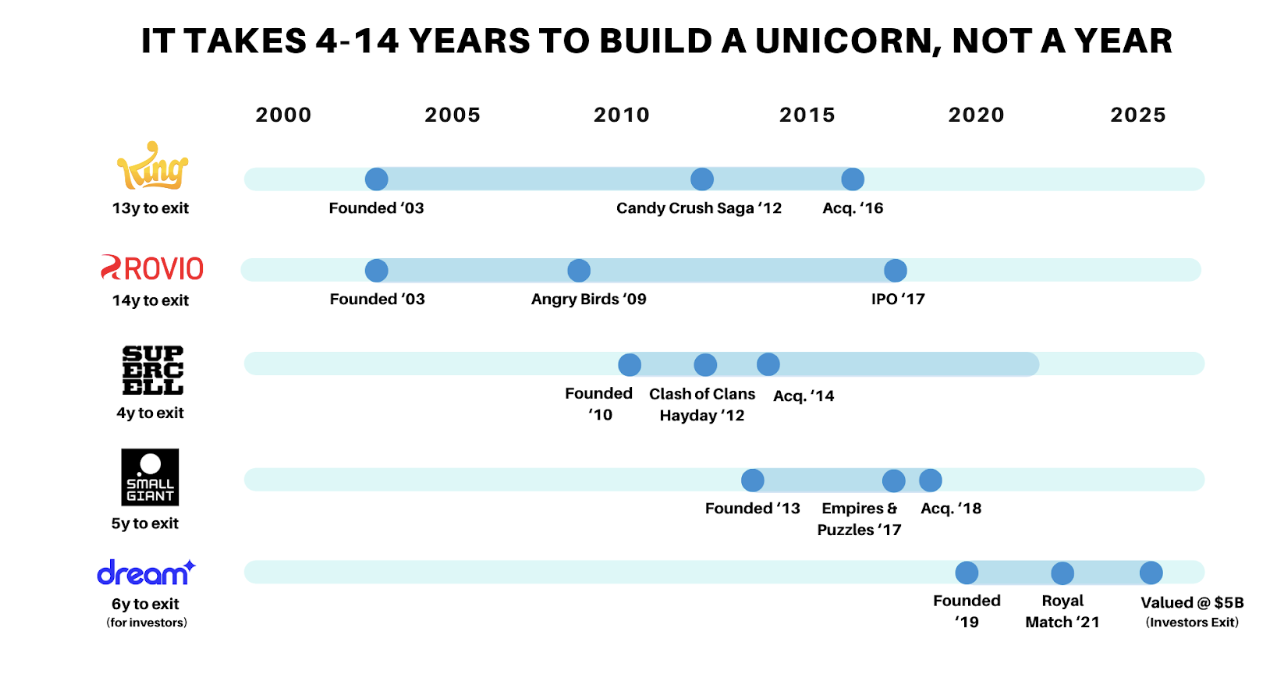

Let's look at some gaming unicorns we all admire:

King (founded 2003) developed roughly 200 browser games before Candy Crush Saga became a phenomenon in 2012—a full 9 years after founding! Acquired by Activision Blizzard in 2016 for $5.9 billion.

Rovio (founded 2003) experimented for years before Angry Birds took flight in 2009—6 years after founding. Went public in 2017 at a $1 billion valuation.

Supercell (founded 2010) started with the vision of making cross-platform games. Their first title Gunshine.net (web browser and Facebook MMORPG), didn’t work out. They later launched Clash of Clans and Hay Day in 2012, nearly 2 years after founding. Later acquired by Soft Bank in 2014 and then by Tencent in 2016 for $8.6 billion.

Small Giant Games (founded in 2013) didn't see any success until Empires & Puzzles took off in 2017. That’s 4 years after founding. The company was acquired by Zynga in 2018 for $700 million.

Dream Games (founded in 2019) launched Royal Match in March 2021, 2 years after founding, and it took them several years of careful development and testing to create the dynamics that made it a hit. Recently valued at $5 billion in 2025.

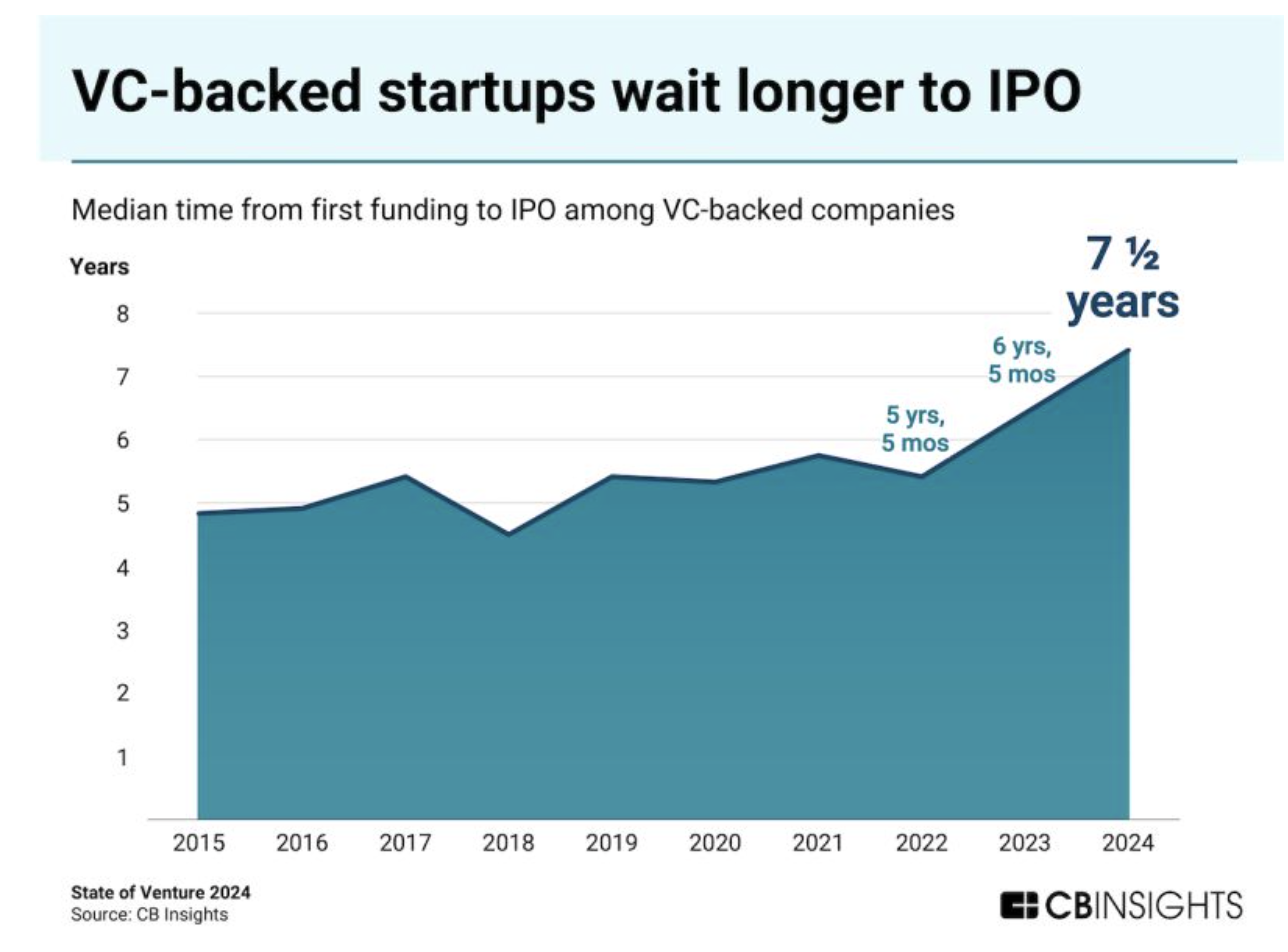

The 1-year cliff and 4-year vesting schedule became standard during the mid-2000s when money was cheap and acquisitions happened fast. In 2005 the median time to IPO was 5.6 years (from first funding) while the median time to acquisition was 4.6 years.

That economic reality is gone: the median time from first funding to IPO is now 7.5 years. Yet, somehow, the old vesting schedule stuck.

Why the 1-Year Cliff Can Kill

1. The Founder Breakup: You Aren’t The Only Exception

We've seen this story happen more times than we like: an early departing founder walks away with significant equity, while those remaining are left holding the bag and now have to plug the gap with a combination of more work and/or finding additional talent to join them as early employees. This requires offering equity from the founders’ pockets or an unplanned use of the employee stock option pool (ESOP).

In other words, if a co-founder leaves, it’s the other founders who are left in the trenches that will get diluted. Not to mention that the exited co-founder can potentially hurt your next financing round by owning “dead equity”.

It's not fair, but it happens a lot:

14% of failed startups attributed their death to team issues. 7% said the failure was due to team disharmony. You tell me the difference.

We estimate that 15%+ of companies have had early founder departures that take place after Year 1

The danger zone? Months 9-18, when the cliff approaches and tensions peak

"The Play partners advised me to do a 2-year cliff. I didn't listen, and our lead investor didn’t ask for it either. BIG mistake. It was my first startup, and our co-founder was struggling, but I was convinced he'd improve. By month 13, it was clear he couldn't deliver on the roadmap and was creating a toxic environment, but the cliff had passed. It was not an easy breakup. We wasted months negotiating his equity down, and it was a tight-rope walk because legally, he was entitled to the vested equity, even if it was unfair to the rest of us. Honestly, a 2-year cliff would have saved us tens of thousands in legal fees and hundreds of hours of stress. It drained me emotionally,"

Brad*, first-time founder and CEO of a mobile studio.

2. Dead Equity That Haunts Your Fundraising

“Everyone enters into a startup with ambitions. It’s only through running a company together you find out if those ambitions align. Unfortunately, we found that priorities did not align, with a co-founder not committing to the company’s best interests. You need time to figure that out and a year is too short in my opinion. When my co-founder left after a year or so, she had vested a lot of equity. Our board and other potential lead VCs we spoke to told us we had to get her dead equity way down for a new fundraise to happen,"

Jennifer*, CEO of a gaming studio.

This “dead equity” or, more kindly, "zombie equity" is the undead ownership stake that won't die and won't contribute any further. A departed founder with a big chunk of equity who's no longer operational but still lurking on your cap table can scare away new investors and can block follow-on rounds or demand outsized payouts when you least need the drama.

3. First-Pivot Punishment

Most year-one products don't hit it out of the park. Without extended vesting, founders lack "skin in the game" for the second and third iterations that usually crack product-market fit.

When your first game isn't hitting the numbers you hoped for, you need everyone all-in on the pivot. The 1-year cliff creates a perverse escape hatch right when your team should be doubling down.

Getting a startup off the ground is soul-breaking. The failures are inevitable. It’s extremely tempting to just go back into a nice, cushy job after being smacked around by reality. The two-year cliff disincentivizes this. If you leave early, you’ll leave with the experience but with none of the shares.

The Origin of Play's 2-Year Cliff

This isn't just investor theory; it comes from founder experience. Play's founding partner Henric experienced this firsthand as a founder at Nonstop Games. When investors pushed for a standard 1-year cliff, Henric and his co-founders counter-proposed two years. They'd already weathered demo failures and knew they needed commitment through their crucial second-year pivot.

"Everyone seems fully committed—until they’re not. When you sit down with your co-founders to sign a deal that includes a two-year or longer cliff, that’s when true commitment is revealed. It’s one of the most effective ways to separate those who are genuinely in it for the long haul from those who are just testing the waters,”

Henric Suuronen, Founding Partner, Play Ventures

What started as founder protection became Play Ventures' standard practice. We've now invested in about 100 companies since 2018, and our experience is clear:

Not a single founder (who stayed) regrets the 2-year cliff

Several founders have regretted not implementing it

True company value creation happens over several years (not just at the start)

Here's how it actually protects you:

Leaver Negotiations Start at a Fair Place

When a founder does leave (it happens), a 2-year cliff gives remaining founders:

A cleaner cap table for follow-on financing

Buyback negotiations start at a reasonable percentage reflecting early contribution and the remaining work to be done, and the journey ahead

“So much can happen in the first two years of a startup. The first year was pure elation and excitement, but the real trouble started in year two. Things got really tough, one of my co-founders decided it wasn’t for him anymore. Thank god we had a 2 year cliff. It made negotiations with my exiting founder quick and painless. Everyone parted on good terms, no resentment or hard feelings, and we still had a clean cap table and could go on"

Ben*, founder of a mobile game studio.

It's a Powerful Commitment Check

One founder balked at our 2-year cliff term. We passed on the deal. Months later, after successfully raising elsewhere, he left for a big corporate role, with a large equity chunk of the company. The remaining team had to carry on and deal with the new and unhappy investors.

The 2-year cliff weeds out "fair-weather" founders before they burn goodwill and resources. It’s a good filter for founders and for investors.

Armor Against Reset Vesting

Later investors often demand cliff resets during financing rounds. With the 2-year approach already in place, your founding team has demonstrated extraordinary commitment, making it easier to re-negotiate on unnecessary resets in later rounds.

Good for Founders AND Investors

Let's be real: yes, a 2-year cliff also helps investors put in fresh capital. We avoid situations where we give you a check based on the founding team only to see one of the founders ditching early (for whatever reason).

This alignment of incentives is good: your success as a founder and our success as investors become intertwined. We both need the core team to stick together through the inevitable challenges in the early years.

Among our portfolio companies, the pattern is clear: teams with 2-year cliffs have more stable companies that can better weather the inevitable pivots and the unfortunate early founder departures.

Embrace The Cliff

The 2-year cliff comes across as unfair at first. You’re setting up a company, yet for two years, you don’t actually get any of the shares. Crazy, right?

But when you match this practice against reality, it makes a lot of sense. Gaming startups typically need over two years to find their stride. Your vesting schedule should reflect the reality of building a gaming company, especially in today’s environment.

And hey, if you want to chat more about this or any other term sheet quirks, my DMs are open (Find me on X @ppphyl or just email me directly.