2021 Predictions #4 Contenders Throwdown for Supercell's Mid-Core Crown

This analysis is written by my friend, Buğrahan Göker who focused on 4X games, and Yours Truly.

Access all of our previous predictions. Signup for the newsletter. Apply for our Slack group.

Our 2021 predictions have been sponsored by Facebook Gaming.

Facebook Gaming helps developers and publishers to build, grow, and monetize their games. This is done through in-depth research, insights, and case studies as well as innovative marketing solutions and education materials.

Visit Facebook Gaming where you’ll find an incredible amount of insightful, actionable, and relevant information along with tips, tools, and solutions to help you grow your business.

Unless otherwise specified, all the data has been provided by the powerful Sensor Tower and analyzed by the author(s). All revenue numbers show net revenues. Data from China, Korea, and Japan are excluded as this analysis focuses on Western markets only.

Finally, please take the numbers presented with a giant grain of salt. They are meant more for trend analysis based on estimations, rather than an exact numbers.

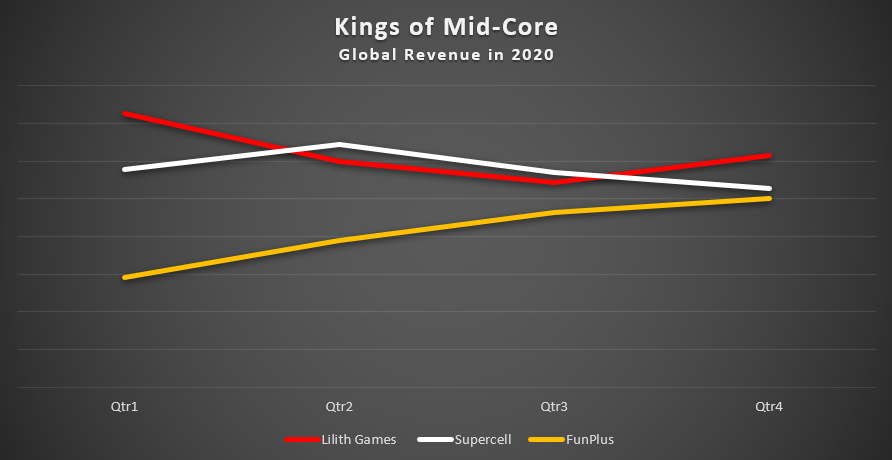

This analysis will give you a full overview of the Strategy games genre, which is the second-largest genre in the Western markets after puzzle. But before we break down the market, the main players and give out our predictions, I’d like to present the two graphs that led to the title of the post. The two graphs below show that competition for supremacy of Mid-Core in the Western audience is a tight race between Supercell and FunPlus.

When excluding China, revenues for Supercell and Lilith look more stable while FunPlus’ shows the same impressive growth.

Lilith is the dark horse when zooming out and looking at global revenues. Given the current trajectory, Lilith will surpass Supercell by the end of Q1 of this year. And as the year progresses, Lilith’s slate looks extremely strong with one game scaling in soft-launch and another very promising shooter title set to launch in 2021.

The way things are looking, we will be crowning the new king of mid-core (in the West) by the end of the year, if not sooner - unless our friends at Supercell launch another billion-dollar game. A scenario that is more than likely.

Looking at global revenues, Supercell and Lilith both declined during the frothy 2020 while FunPlus made incredible gains.

Strategy Games in 2020

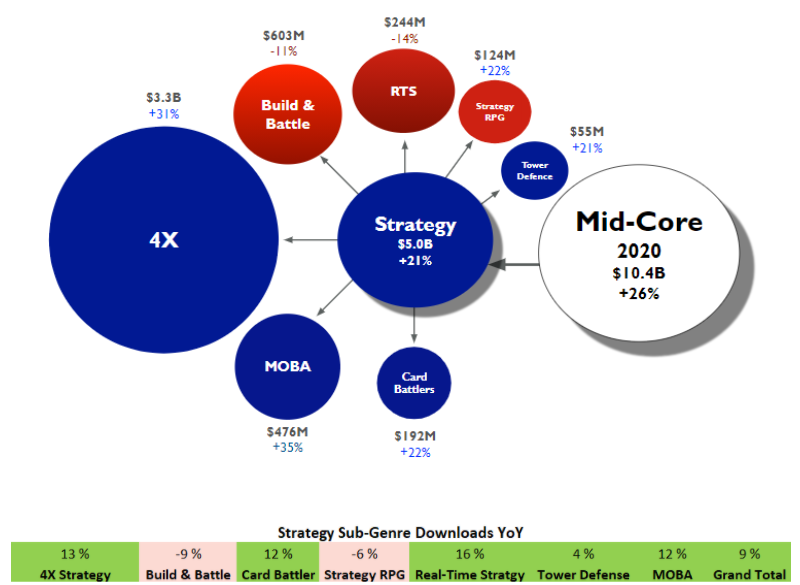

Strategy games, which are composed out of 7 sub-genres, generated $5B in net revenue during 2020 growing IAP revenues by 21% while the downloads were up 9% year-over-year. This makes the genre second largest on mobile in (outside key Asian markets) after Puzzle games. Strategy games also represent nearly a half of all Mid-Core revenues.

Just like last year 4X continues to dominate the strategy genre making more than the rest of 6 sub-genres combined. The growth was driven mainly by existing titles scaling up as the overall downloads in the 4X sub-genre grew only by 13% YoY. In fact, we saw 13 4X games earning more than $100M in gross revenue during 2020.

While today's Game of War is little more than a profitable legacy title, the game was pivotal to growing the 4X sub-genre to what it is today - a $5B sub-genre on mobile in the Western markets.

The second largest sub-genre is the good and old Build & Battle. Supercell’s Clash of Clans is by far the dominant title in this sub-genre as it declined, so did the sub-genre as a whole. Though in this case the dominant titles declined less than other key titles in the sub-genre. Castle Clash by IGG, War Dragons by Pocket Gems and Art of Conquest by Lilith all came down between 15 to 35 percent compared to 2019. By all accounts this genre is matured to a point where it could use a massive innovation to both the progression mechanics and social gameplay. After all, these games have a fun combat core brutalized by ever increasing timers which just simply don’t work in the modern mobile market.

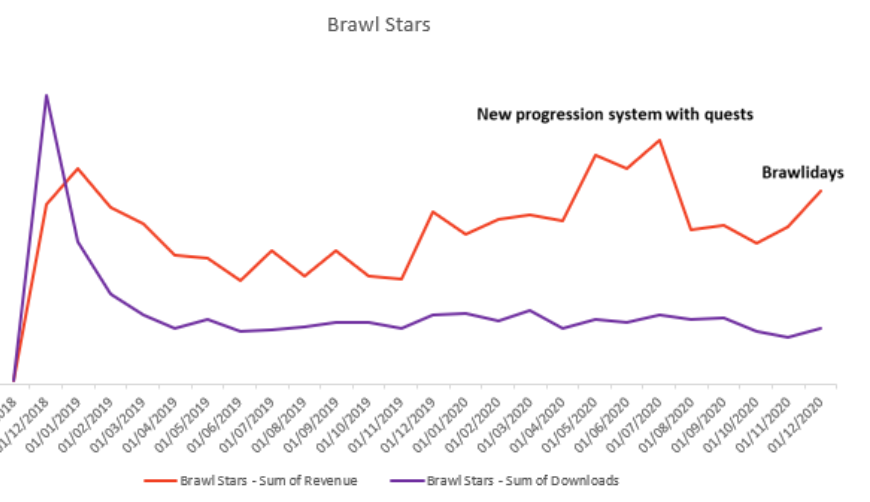

While we’ve been constantly sceptical about the potential for MOBAs outside key Asian markets the sub-genre continued to grow at the highest pace in the genre. The growth was driven by the growth of the two top titles, Mobile Legends and Brawl Stars as well as the launch of League of Legends Wild Rift. The growth number you’re seeing above would be even more considerable, had we included the revenue from Korea and China, which contributed significantly to Brawl Stars 2020 run-rate. But don’t worry, we will have a proper analysis of the genre and the game with a look at all key markets as a part of this analysis.

Real-Time Strategy (RTS) as a genre has always been very difficult to enter due to Clash Royale’s dominance. In 2020 the genre was a true disappointment with Clash Royale’s rapid decline continuing while new entrants with interesting take on the core and the meta, such as Battle Legion, failed to scale despite a great start. The only true bright spot was Art of War, which despite prototype level production quality has scaled up to over 5M in net revenue a month with no stop in sight!

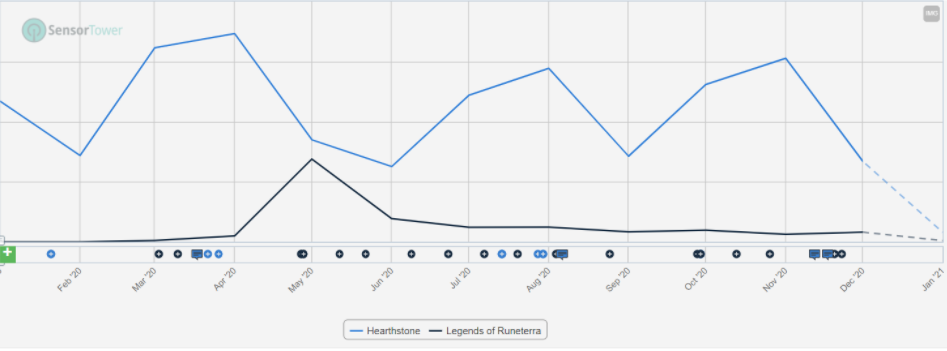

Card Battlers used to be a sub-genre led by Hearthstone. Then Yu-Gi-Oh came along. It grew the market and became bigger than Hearthstone on mobile. And while we were expecting Magic the Gathering, Gwent, Legends of Runeterra and Elder Scrolls Legends to challenge Hearthstone directly, there was a WWE SuperCard game that grew 30% in 2020 and is now the second largest game in the sub-genre. And all those auto-chess games that seemed to be clear substitutes for Hearthstone. Well, with non-existent monetization and progression they never even made a dent.

WWE Super Card close-lined Hearthstone in 2020 to become the second-largest card battle game in the West on mobie after Yu-Gi-Oh. But please keep in mind that Hearthstone is cross-platform title making likely over 80% of its revenue on PC.

Just as predicted last year, Strategy RPG grew in 2020. Though the growth is different than we imagined. Top titles, such as Game of Sultans, declined as new titles entered the competition. This doesn’t speak well about the overall potential of the sub-genre. When looking beyond the numbers into actual player experience, these titles continue to be poorly accessible. They confuse a set of menus, tasks, and resources that instead of getting the player into the groove of things manage to frustrate the player to uninstall the game after a couple of sessions. Until one of the developers takes a page out of interactive narrative games, this genre will remain but a niche in the Western markets.

Last year, we predicted that the Strategy RPG sub-genre may open up to female audiences with female-focused themes. Royal Romance was one of the frontrunners among female players. The game adopted a traditional Chinese dynasty theme but with a stronger emphasis on love and relationships. Demographics according to Sensortower is showing that 90% of players are in fact female.

Tower Defense was a tiny genre up until early 2020 when Arknight launched and scaled to very impressive revenues. The game combined RPG with traditional tower defense gameplay resulting in much better monetization. While we expect similar titles to launch during 2021, the next surge will come from synchronous tower defense battles like Tower Duel and numerous similar titles. While this may look new to most players, it is in fact a game type that has been extremely successful in Korea. We’ll see if the game style can resonate in the West. There is no reason why it couldn’t.

PvP Tower Defense games will be the new hot thing in 2021. This is exactly the game that (in our opinion) Supercell should have made. It will be interesting to see if Supercell jumps on this trend or chooses to ignore it. Based on historical data, our bet is on Supercell skipping this one as well and focusing on something new.

Supercell Failed to Capture Growth in a Booming Market

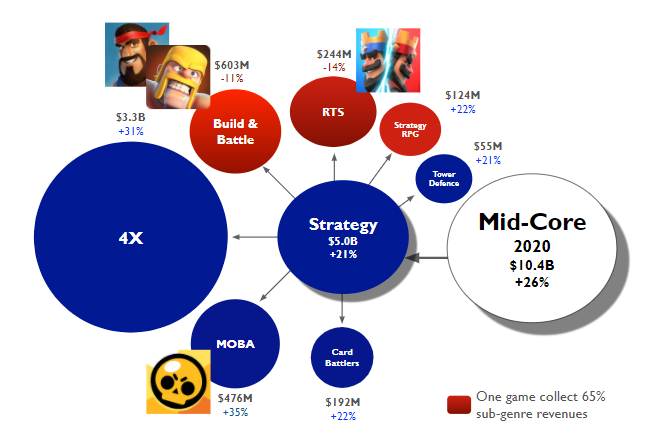

Supercell dominates two sub-genres (Build & Battle, RTS) and is extremely strong in one (MOBAs)

Supercell continues to control three of the Strategy sub-genres. Clash of Clans takes nearly 70% of all Build & Battle revenues. Clash Royale clears 72% of all RTS (real-time strategy) revenues and Brawl Stars takes an honorable 60% of all MOBA incomes. Over the years, Supercell’s portfolio has become slightly more balanced, with other games than the Clashes bringing in a more significant portion of the revenue. Yet while Supercell’s dominance in the three subgenres is largely unquestionable and remains unchallengeable, there are some concerns that can’t go without mentioning.

Supercell’s portfolio is more balanced and not so heavily reliant on Clash IP, which still brings over 50% of the revenue.

Further examination of Supercell's portfolio shows that despite the rising tide driven by the lockdowns, only Brawl Stars was able to grow in par with the growth of the market. And while we praise Brawl Stars for the amazing updates and the great community driven growth strategy, the real reason behind Brawl Stars’ growth has been the fact that the game launched in China. The launch was incredibly successful. The problem is that the game has shown very poor sustainability in the Chinese market with monthly run-rate dropping by over 90% inside a few months after the launch. In fact, without the China launch, Brawl Stars would show only 3% year-over-year growth while the rest of the mid-core market grew over 30% in a year. Not to mention that Brawl Stars was not published by Supercell in China, meaning that they likely got a far smaller piece of the added revenue. Though the publisher in China was a Tencent portfolio company, which means that no Renminbi went past the parent company.

Brawl Stars’ revenues (excluding China, Japan, and Korea) show the impact of updates and also how infrequent these impactful updates are. Supercell’s Achilles’ heel is to keep up with what is expected from a modern top-grossing game. Imagine updates like Brawlidays rolling at monthly if not bi-monthly schedule instead once in 6 months like they do now…

Clash of Clans was able to hold off a more significant decline with a wildly successful end-of-year update. Without the end-of-year update, we would have seen a much more significant decline for the game’s YoY revenues. Boom Beach remained stable and has been clearly put on lean/automated live ops after the massive mid-2019 update failed to invigorate the game.

The real blow has been the fall of Clash Royale. The game has failed to see an uplift ever since mid-2019 when the battle pass was first introduced into the game. Clash Royale’s gacha driven collection economy with a fairly limited amount of content has been evidently too shallow for a battle pass leading to long-lasting impacts to a game’s revenue stream. Watch our full analysis of Clash Royale vs. Clash of Clans battle passes.

Superecel’s revenues are down only 4% year-over-year. But if you consider that the mid-core market grew by 30% during the same time period, that decline gets harder to justify.

According to the Sensor Tower data, Supercell’s revenues are down only 4% year-over-year. But if you consider that the mid-core market grew by 30% during the same time period, that decline gets harder to justify. The launch of Brawl Stars in China helped out a lot. Without it, the decline would have been 10% YoY. But perhaps the most worrying thing is that this is now the 5th year in a row that Supercell’s revenues declined, and no matter how much we respect and look up to the company you can’t just brush it off.

Supercell’s playbook from 2012 to 2017 was unbeatable. As the mobile market grew, Supercell grew faster and was able to ship one billion dollar game after another with tiny teams. Yet this playbook hasn’t worked in several years now. Top-grossing mobile games are ever-bigger with constantly improving production values and unrivaled live services making the games feel fresh every day. This means that the teams behind these games are bigger. And for a company that has its ethos tied to small teams, growing the team sizes seems to be a very big decision that is not made lightly.

But let's have the right perspective here. The decline of single-digit doesn’t make even the smallest dent in Supercell's massive war chests. The cost structure is likely among the best in the world due to the company has always been very conservative towards growing the headcount. And because the company is private, the long-lasting decline won’t affect stock price and thus create some retention problems with key talent like it would in a public company. After all, talent is the key resource of any gaming company and Supercell has arguably the best talent pound-for-pound.

So what are our predictions for Supercell in 2021? In short: we expect big changes.

IDFA depreciation will not have as big of an impact on Supercell, which hasn’t been on the forefront of modern user acquisition in nearly a decade. The company’s portfolio is filled with legacy titles that operate extremely profitably with very little to no user acquisition. And with new titles Supercell has invested in brand building, influencers, and events.

Despite not taking a shot from the IDFA depreciation, we expect that revenues will continue to decline and will be down around 10% compared to last year. To turn this around Supercell needs to find a new gear with their updated cadence - and it’s already overperforming given how small the team sizes are compared to the competition.

We expect that the changes in the leadership of the company will continue more rapidly as several of the early employees and perhaps even founders will depart. These people took the company to the moon and beyond during the last decade. Now the company has clearly matured and the difficult year in lockdown has likely affected the priorities of many people.

As the leadership evolves we will likely see Supercell making more strides towards larger team sizes. This will add some hierarchy and affect the company culture that has been cemented around small teams.

As the company culture evolves, more employees will choose to start new companies, which Supercell, in turn, will invest into. So as a whole, the evolution of Supercell will boost (once again) one of the best ecosystems for making mobile games aka. Helsinki

Here’s a caveat though. We know that Supercell can deliver a knockout punch in the form of a blockbuster game like no other developer in the World. If Supercell ships a hit game in 2021, the evolution of the company will slow down significantly. But then again, if Supercell delivers another game that fails to pass the soft launch phase, the company’s transformation will likely follow according to our predictions.

For more insights, please read 10 Years of Excellence - Deconstruction of Supercell. It’s arguably the most thorough analysis of Supercell’s strategy, portfolio, culture, and M&A efforts.

Riot’s Mobile Slate Impressed but Missed

As Supercell struggled to grow with the rest of the market, Riot Games failed to make the expected splash on mobile. The company launched three titles during 2020 with all three featuring its prime League of Legends IP. Yet at the end of 2020, the results were far away from what the company was likely expecting as the cumulative revenue on mobile was around $50M and the installs only slightly over 40M.

With two out of the three titles being cross-platform, it may just be that the disappointment was more on the mobile site and that the games made most of their revenue on the PC side.

Legends of Runeterra

Riot’s card battler is very well executed cross-platform game. Yet the overly careful monetization with lack of ground-breaking innovation bundled with underwhelming downloads is a combo that’s very difficult to overcome (on mobile).

A very polished cross-platform card battler featuring champions from League. Looks much like Hearthstone but is a tad more complicated off the bat with a more Magic-like turn-system as well as heroes that evolve. Nevertheless, the biggest difference is the way players acquire cards - or the way that the game monetizes.

Unlike most card games, Runeterra does not have booster packs. Players acquire random cards mostly through a free-to-play grind-for-XP system with daily and weekly rewards. Players can also acquire specific cards directly via soft and hard currency. However, Runeterra took a novel approach to card acquisition by limiting the rate at which players can acquire cards.

In other words, Riot was willing to limit spend depth on card acquisitions because they believed it would make Runeterra more fun. The company believed that by making Runeterra more fun, they’ll retain players longer and make more cosmetic sales. This is following the League of Legends playbook.

Legends of Runeterra has been out on mobile for almost a year now. At launch Runeterra clearly cannibalized Hearthstone but has since then dwindled down indicating that the chosen valiant monetization model is not working. And again, it’s not the execution as Runeterra received Apple’s Game of the Year recognition.

Riot’s second game ever was Teamfight Tactics. It was extremely impressive how quickly Riot reacted to the early signs of auto-chess fever in 2019, given that it had been almost a decade since they last shipped a game. Too bad that none of the auto-chess games has figured out how to actually monetize the audience.

Teamfight Tactics

Riot showed its agility by shipping the cross-platform Teamfight Tactics in a matter of months! It jumped on the Auto-chess bandwagon beating Valve to the punch. Yet as we know now, the auto-chess bandwagon was going nowhere as not a single one of the auto-chess titles was able to monetize its player base.

Teamfight Tactics is a typical auto-chess game. The gameplay is somewhat like a combination of poker and chess with League of Legends champions as pawns. Once you get into it, it is infinitely complex and extremely difficult. The sessions are all over half-an-hour. There’s no power progression. And the only thing a player can buy is a bunch of skins for their game-board and avatar.

In other words, Teamfight Tactics has a tremendously high entry barrier due to complex and long sessions. And on the flip side, the game offers an extremely unappealing battle-pass. As a fan of the game, I never felt inclined to purchase it once - let alone repurchase with the new season. And while the season updates have invigorated the game by totally shuffling the meta, the team has not invested enough to improve engagement with features like leaderboards and clans. The game lacks a feeling of meaningful progression and feels unsocial on touchscreens. As long as these two elements persist, TFT will have challenges monetizing, despite offering a great core gameplay experience.

Why You Shouldn’t Make a MOBA for the Western Audience

MOBAs are very difficult to make, operate and monetize. Yet they are not that difficult to get greenlit because of the multi-billion-Dollar success of Honour of Kings. And it’s also not that difficult to get the talent to build these games as we developers want to make MOBAs because we love playing them on PC. But what is confusing is that MOBAs continue to get greenlit despite no evidence that these games could succeed in the Western markets.

Arena of Valor, which is the Western version of Honour of Kings, failed in the Western markets even though it featured perhaps the most iconic Western champions you can find down Superman and Batman.

While it’s proven that the MOBA core has not resonated in the Western markets on mobile, both League of Legends and DOTA2 are highly popular with the PC audience in the West. So there’s a clear audience for these games and the assumption is that you’d need to make a game with lots of very familiar characters. That’s where MARVEL IP comes in and the player research team has a field day proving that this is a slam dunk and a sure hit. That when asked players who play MOBAs or who are new to MOBAs they’d both love to enter the arena as Black Panther, Hulk, or Iron Man with their mates and wreak havoc.

And while the IP is very expensive to both acquire and operate, what further supports the business case is the assumption that MARVEL games should in theory drive organic installs while offering low CPIs. Not to mention that MOBAs are very streamable, so in addition to all the free installs, the game will also grow with support from influencers - and perhaps even esports.

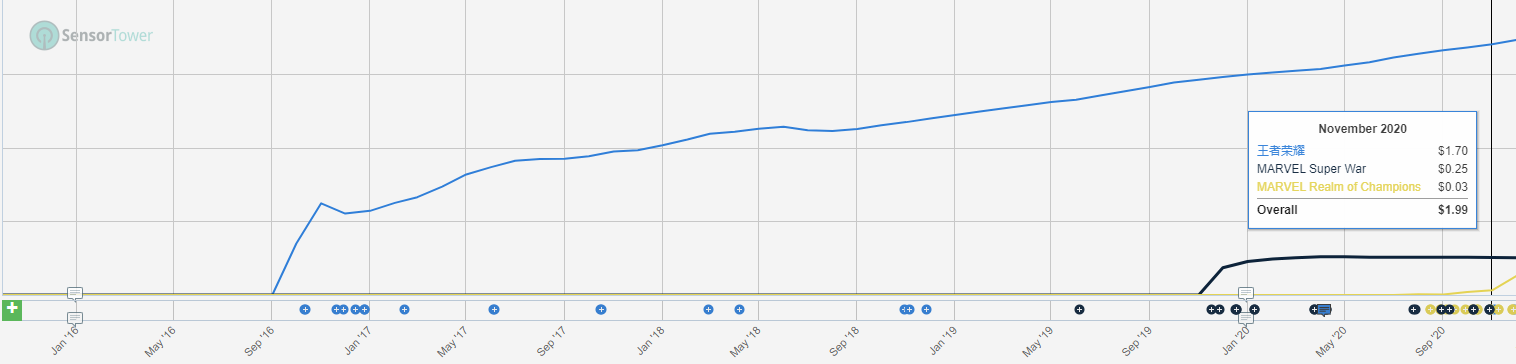

The RPIs (rev per install) for the Arena of Valor outside China are quite low, despite slowly increasing over time as the download volume dwindles down. The RPIs for Marvel Super War were alarmingly low - as were the installs that reached only 15M to date. Kabam’s Marvel MOBA (more of a brawler) is yet in soft-launch but given these examples, it’s hard to see that game reaching the lofty expectations.

Luckily we don’t have to hypothesize anymore. Two different MARVEL MOBAs entered the market within a year. Super War is more of a traditional MOBA from NetEase while Realm of Champions represents a more casual “brawler” version. Super War, which is launched globally boasts around 15M installs in a year and made a fraction of a Dollar per install. These are, unfortunately, catastrophic numbers for an IP that charges a minimum guarantee bigger than most companies spend to market their game. Not to mention that just the production costs for a high-quality MOBA are likely around $20M. Realm of Champions from Kabam, while still in soft-launch, will be the latest MARVEL MOBA to test the waters, but based on all the data available, it’s hard to be overly optimistic about the game’s chances.

Personally, having played extensively all of the key MOBAs on mobile, I sadly don’t see a turnaround for Kabam’s version either. The gameplay is already quite casual and in theory, they could pivot it closer to Brawl Stars’ version of arcade brawler-MOBA-shooter. Though given the art style employed in Realm of Champions, this pivot is only a theoretical opportunity at best.

I believe that there’s a sound case why MOBAs, which look absolutely fantastic on paper, have a slim to none chance to succeed in the West - even with the support of the best IP the world has to offer. But what if you launch a mobile version of a PC MOBA with a massive existing and lapsed audience? Surely that would work! It could be that MARVEL is just too “casual” of an IP…

Wild Rift is the first mobile game Riot has ever shipped. And it is a truly fantastic MOBA experience on touchscreen devices. Yet despite nearly flawless execution, the game’s performance looks very weak, supporting the claim that the Western audience just doesn’t want their MOBAs on their phones.

League of Legends Wild Rift

It is understandable that the expectations for the mobile version of the biggest MOBA in the World were at an all-time high. After all, Tencent’s Honour of Kings, the most successful MOBA on mobile is likely to cross 10B in life-time revenues in a year or so. Yet we at Deconstructor of Fun were far more conservative in our expectations. The reason being that none of the traditional MOBAs have found any sustainable success in the West - and it’s not because of the lack of trying either. Even Arena of Valor, the Western version of Honour of Kings, made less than $20M in life-time revenues in the US.

The positioning for Wild Rift was clear. It’s a more action-packed League of Legends aimed likely first and foremost for those who are new to the franchise or who have lapsed from the PC version. With an active audience in the tens of millions, it makes a point to do a game for those watching the streams and not necessarily participating anymore.

Looking at the RPIs, Wild Rift is on par with Arena of Valor’s numbers when it launched - and that’s a game that couldn’t scale up in the West. This indicates that the book on Wild Rift is closing fast as the expectations for the golden cohort were likely on another level. And Riot has also clearly invested in user acquisition with ads running constantly on all the major channels. Yet despite the UA investment, they reached ‘only’ 15M installs during the first month. This must be a major disappointment for a game that is actively played by 100-120 million players worldwide.

Launch in China could turn the Wild Rift case around, but as we know that can take easily two years from now. And then there’s the Honour of Kings which dominates its turf making regularly over 200M a month.

So what are our predictions for Riot on mobile in 2021?

All three of its games will remain niche titles with yearly portfolio revenue well below 50M a year

Riot will keep supporting the games with a steady stream of updates as two of them are cross-platform and likely making a significant portion of their relatively modest revenue outside mobile. Wild Rift will hold on to the hope of one day launching in China and making it big there.

Riot won’t launch other mobile titles in 2021

What could Riot do - in our very humble opinion:

Adopt fair monetization models that are proven to work instead of trying to create games with what one could describe as apologetic monetization systems. The company is entering a new market with an audience used to traditional free-to-play systems. Bending over backward for the vocal minority of their player base doesn’t seem like a sustainable way as the demands to de-monetize will arguably never ease-off. And there are plenty of examples of RPGs that have strong monetization bundled with a great community - for example, Puzzle & Empires.

Launch Valorant on mobile! We bet that his game will be an instant hit in the rapidly growing mobile shooter genre.

Take risks. Make new games that actually feel new. TFT, Runeterra, and Wild Rift were all polished and offered interesting incremental innovations. But they didn’t feel fresh in any shape or form. It was more like game X with LoL champions. With the League of Legends providing all the security and the best talent in-house, you’d expect Riot Games to be bolder.

Explore, Expand, Exploit & Exterminate

Machine Zone’s Mobile Strike is one of the genre defining games in the 4X sub-genre. It proved that reskin strategy in the sub-genre is not only a valid approach but the right approach due to each game having very high ARPPU, relatively low DAU and never satisfying demand for those high-spenders.

4X sub-genre (eXterminate, eXplore, eXploit, eXpand) is the biggest sub-genre in the Mid-core category with $3.3B revenues and 31% growth YoY. Even though it lost its position as the largest sub-genre on mobile to Match-3 games, 4X games continue to make up one-third of the mid-core market. Not to mention that 4X games represent more revenue than the rest of the strategy sub-genres combined.

4X continues to be an extremely lucrative opportunity for publishers with deep war chests, strong technical capabilities, outstanding live service skills, and robust user acquisition teams. Success in 4X is less dependent on radical differentiation compared to other genres. Noticeable incremental innovation in product and or marketing bundled with excellence in performance marketing and live services can deliver an appreciable share of the booming market.

4X Games and Publishers in 2020

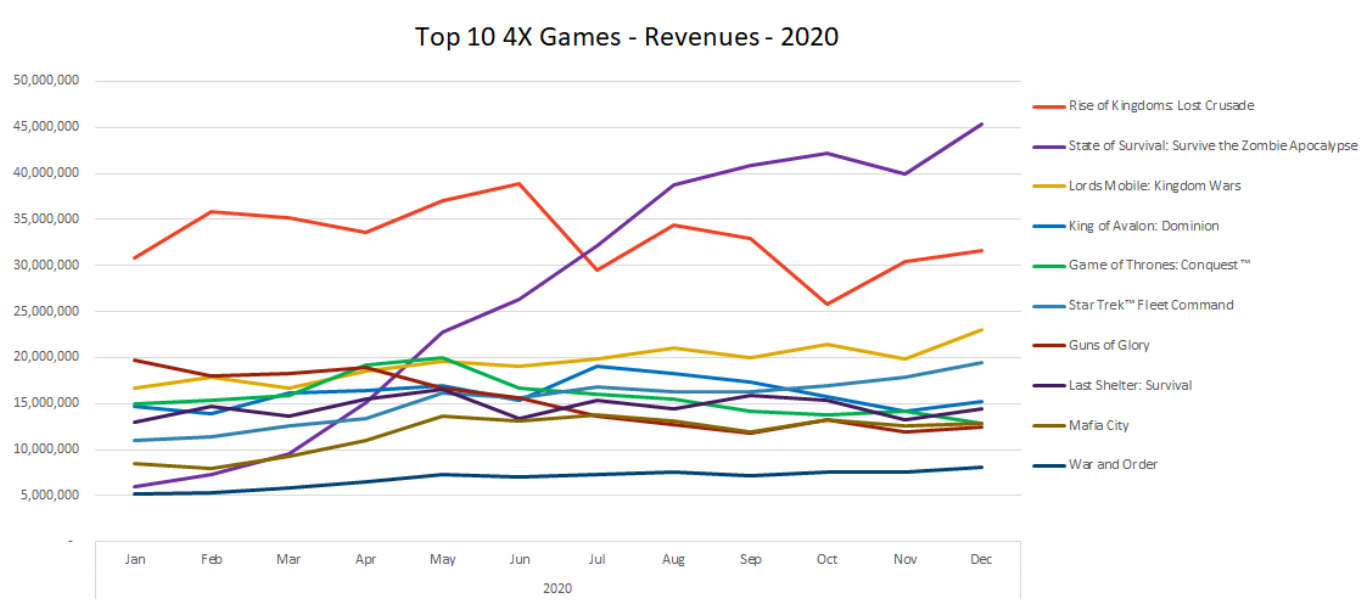

FunPlus’ State of Survival was the monster hit of 2020. Lords Mobile from IGG and Star Trek from Scopely experienced some nice growth. Liliths’ Rise of Kingdoms seems to have hit it’s ceiling in the West. Though what is not shown is the global appeal of Rise of Kingdoms as the game cleared 300M in net revenue from key Asian markets that are excluded from the graph making it by far the biggest 4X game in the world.

4X sub-genre continues to be highly fragmented, which opens up opportunities for new games and companies building portfolios for strategy games without cannibalization.

Korea, Japan, and China excluded from the graph above.

The revenue continues to be evenly distributed among top titles, not dominated by a handful of games as seen in many other genres. Even though Lords Mobile dropped one more position in ranking this year with only 4% growth YoY compared to the whole sub-genre growing 31%, 2020 was a phenomenal year for IGG. Lords Mobile became the 3rd 4X title that surpassed $1Bn cumulative net revenues in February.

Chinese developers continued to dominate the 4X sub-genre by taking more than 75% of all 4X revenues in 2020. There were only 4 games that managed to break into the Top 20 and all four newcomers were games from seasoned chinese developers (FunPlus, TOP Games, Long Tech and Leyi Network). Why Chinese developers are performing better in 4X while Western developers are struggling to break into?

4X Games require a high level of technical expertise

Asian developers are at their strongest in meta-game design, which is essential in 4X games

The level of innovation in the genre is low, which suits developers who are good in reverse-engineering.

On the flip side, experienced Western developers look down on reverse engineering games and always want to add perceived product improvements

4X game development requires large team sizes, which contrasts with the development style of most Western mobile developers - though this is changing as the market is maturing

Lilith wins in all the markets

As we predicted in our last year’s post, Rise of Kingdoms by Lilith Games became the top-grossing title this year with $400M in net revenues and 51% YoY growth. When it was launched in late 2018, Rise of Kingdoms (RoK) stood out with its highly appealing theme that was strongly influenced by Civilizations. But it wasn’t just marketing, where the game stood out. RoK brought novelty to the subgenre with its combat system that allowed unrestricted movement of armies on the map. This incremental improvement allowed simple things like parking your army to a point on the map. This little thing allowed significant strategic depth compared to rival titles.

Rise of Kingdoms is making well over a billion a year. What’s incredibly interesting is the global appeal of the game with significant revenues coming from literally all key markets in the world. Then again, no wonder, given that players can choose to play with real-life historical characters from all the current and past empires of the world. And naturally, those historical characters enable highly localized marketing campaigns.

On top of that, Lilith managed to keep the game fresh by continuously adding unique events, new features, and new layers of competitive gameplay for the elder players. Lilith is also following a similar strategy that brought success to its competitors and published a new 4X title called “Warpath” in a completely different setting (World War 2 instead of the historical fantasy theme of Rise of Kingdoms) to expand its player base to a new audience. The game is currently available in Google Play and expected to be released also on iOS devices in March,2021. The early performance looks extremely promising and most likely will break into the Top 10 in the second half of 2021.

Lilith’s latest strategy game is currently available in Google Play and expected to be released also in iOS devices in March,2021. The early performance looks extremely promising. We expect this game to break into Top 10 in the second half of 2021.

FunPlus - The biggest winner of 2020

Even though Rise of Kingdoms topped up the charts in early 2020, FunPlus took over the crown in the second half by scaling up their latest title “ State of Survival” aggressively throughout the year. State of Survival surpassed its predecessors, King of Avalon and Guns of Glory, in terms of first 12 months performance by reaching record-high monthly revenues above $40M. As a result, FunPlus increased its annual revenues from $540M to $850M in 2020 by growing both State of Survival and King of Avalon as well as securing the title of number one publisher with 22% market share (from 18% in 2019).

FunPlus’ State of Survival grew revenues nine-fold during 2020 becoming the biggest 4X game in the Western markets. What makes this title unique is the RPG core game, which adds yet another progression vector to already impressive amounts of elements players can interact with.

Top 3 Western 4X Publishers in 2020

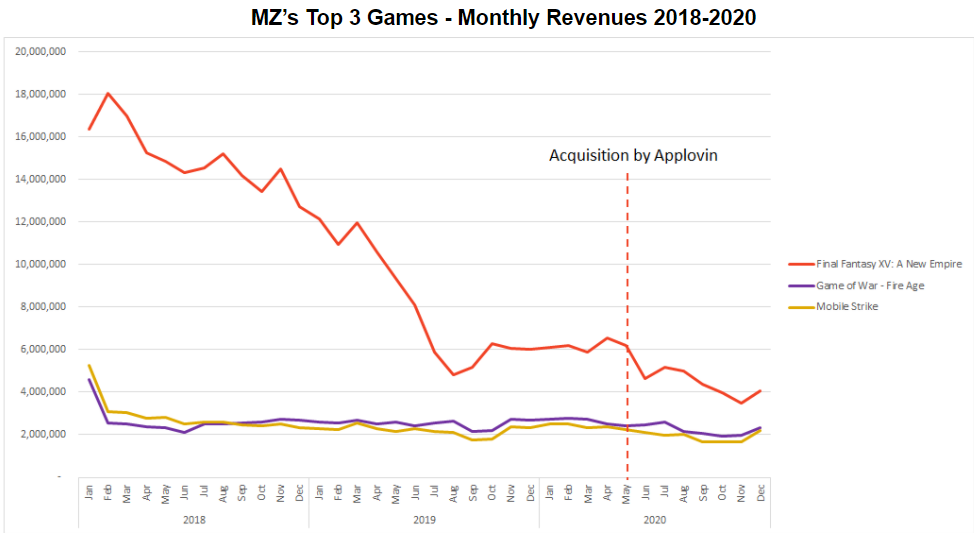

Undoubtedly, the biggest news of 2020 for the 4X subgenre was the acquisition of Machine Zone by AppLovin. The developer of all-time highest-grossing 4X titles such as Game of War and Mobile Strike was acquired by AppLovin in May 2020 with an estimated valuation of $500M. The company was estimated to be worth $5 billion at its pinnacle times in 2016.

AppLovin entered the 4X market through an acquisition of Machine Zone. But there are several steps to take before AppLovin can become a contender in the sub-genre.

Machine Zone was the undisputed leader in 4X game operation as one of the first companies to truly run a F2P game-as-a-service. The publisher perfected performance marketing at a scale in the 2012-2016 era by building up a massive team of media buyers, investing heavily on tools and technology solutions. But as the mobile gaming user acquisition has changed towards algorithmically-optimized campaign management, Machine Zone lost its competitive advantage and lost market share to companies such as FunPlus and IGG that brought more innovative games all while rival Western publishers took on effective IPs to scale up. On top of that, Machine Zone’s outdated portfolio with inferior products failed to modernize. Even though MZ had few more attempts by launching World War Rising in 2018 and Crystalborne (a mashup of RPG and 4X) 2019, none of these achieved the needed level of success.

But while Machine Zone’s new games failed to scale, its legacy portfolio continued to bolster strong long tail revenues. Both Game of War and Mobile Strike steadily made around $5M monthly revenues for the past 3 years with seemingly no marketing support. So despite being considered a ‘failing publisher’ MZ managed to generate $138M in net revenues in 2020 with only 2 million new installs. Today MZ’s portfolio makes up a significant portion of Applovin’s IAP revenue every month after the acquisition.

AppLovin, which started out in 2012 as a mobile marketing company has acquired or formed 12 studios within the last 2 years. Machine Zone was their biggest acquisition up to date and this acquisition can be beneficial for both parties:

Improvements on the performance of legacy titles: Applovin can improve onboarding of legacy titles/make the FTUEs more approachable and attempt to restart UA at smaller scales with the cutting edge expertise they have in performance marketing. This option is highly unlikely.

Capitalising MZ’s knowledge in operating live games: MZ is historically strong in operating live services. Applovin’s other studios and existing titles can benefit MZ’s expertise in live service execution.

Providing extra resources and support for next-gen MZ strategy game: As a part of a vast organization now, MZ can seek extra resources and support to create a modern 4X title backed up by best in class performance marketing.

Use MZ’s oceans of data to build modern 4X titles within other studios in their portfolio. The data from years of building, scaling, and operating 4X games is highly useful for a new publisher who may have the chops to build a 4X game but would have to run endless experiments to learn how to win in the genre. We think that this is the most likely reason for the acquisition.

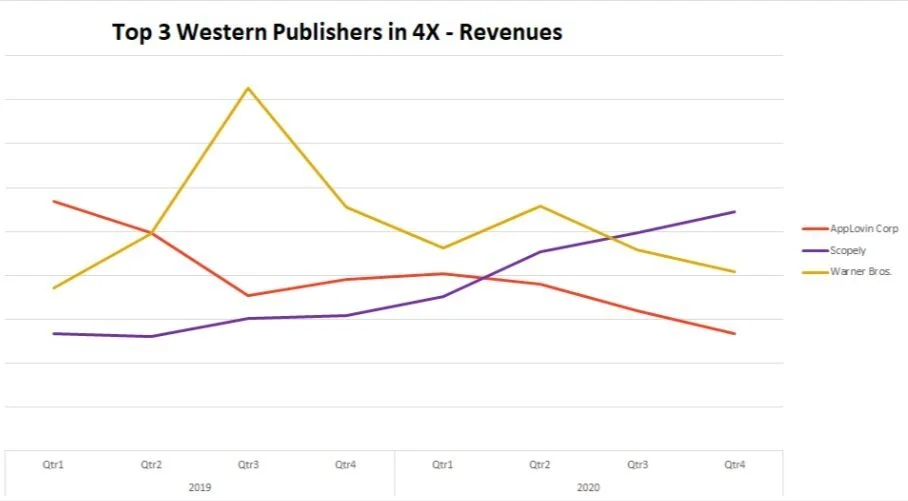

Scopely becomes the biggest Western 4X publisher

Scopely had a good year by growing Star Trek Fleet Command 61% YoY. The company cemented its position in Top 10 ranking and became the best performing western publisher in 4X.

Scopely’s Star Trek Fleet Command has scaled extremely impressively and with new 4X titles in the works, we expect Scopley to become a strategy powerhouse in a few years.

Scopely’s second 4X game from FoxNext, Avatar: Pandora Rising is still stuck in soft launch. The game was originally planned to be globally launched in 2020 but the release date is delayed until further notice. The developers made 8 major updates within the last 15 months and expanded into Tier-1 European countries in August 2020. But Scopely is known to leave no stones unturned as they hunt for their next big hit. In the case of Avatar it looks like they poached the Executive Producer from Warner Bros Game of Thrones game to bolster up their already strong 4X capabilities.

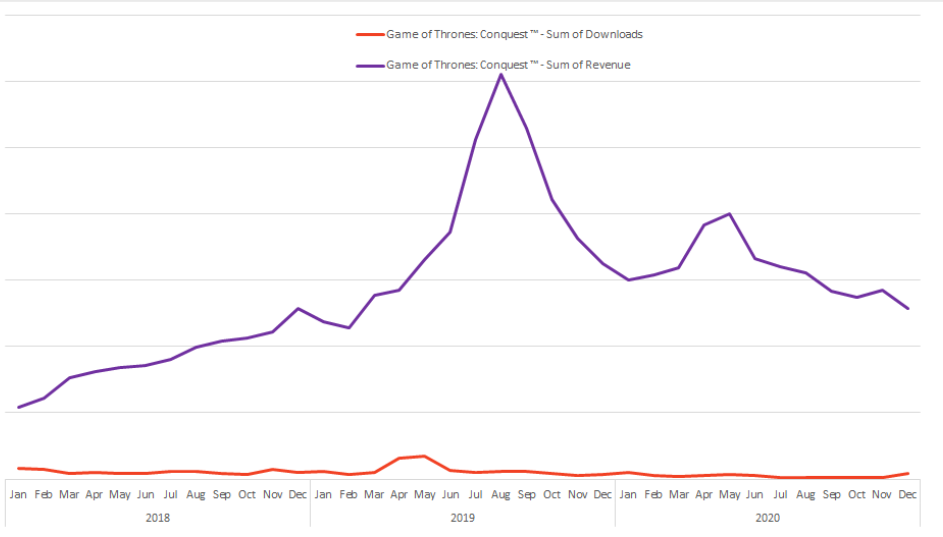

Warner Bros declines and turns to licensing

Warner Bros had a steep decline in both revenues and downloads (16% and 64% respectively) but still managed to generate $190M thanks to the strong long-tail performance from Game of Thrones: Conquest. The company announced a collaboration with NetEase for the development of a new strategy game based on The Lord of the Rings IP. Which seems like the WB is taking a step backward since they already did a Hobbit game with Kabam back when Kabam was the premier 4X publisher in the West.

After the success WB had with their Hobbit 4X game that they licensed to Kabam, the publisher decided to build a 4X game internally (Game of Thrones). And now it seems like they are back to licensing, instead of building on top of the success they worked so hard to aciheve. A very confusing move by all accounts.

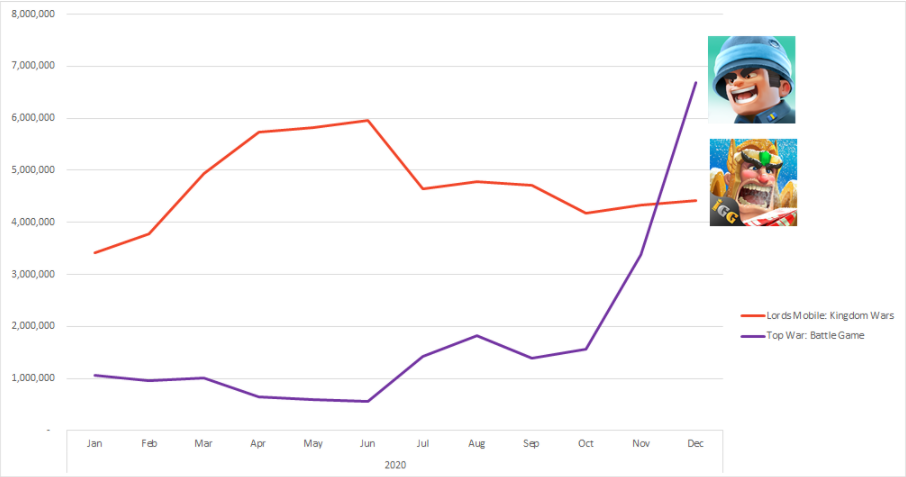

Top War and Evony: Noteworthy Top Runners of 2020

There were 2 titles that caught up our attention from the Top 20 grossing list this year. The first title, Top War adopted the “merging” mechanic popular in the Puzzle genre with an ambition to introduce 4X games to a more casual audience. It includes all elements for a typical 4X game such as base building, PvP, the alliance system, and expansion but with a twist of the simplified and more approachable core. This strategy seems to have worked well considering that Top War was the most downloaded 4X game since November 2020.

Top War and Evony are games that outran the competition with superior marketing. Though Top War did one better and actually merged a merging core with 4X meta.

Here’s how it looks in a graph when the innovation pays off and the marketing clicks.

The second title to mention is “Evony” which was originally launched in 2016. Its publisher Top Games tried to scale up the game several times in the last 4 years (including a Super Bowl ad in 2017) but never managed to secure a stable position in Top 20. But in March 2020, Evony followed up Playrix’s marketing strategy by creating marketing copies around “solving puzzles and saving heroes” and implemented a puzzle oriented gameplay.

Evony took a page out of Playrix’ book and it worked like a charm. The misleading minigame implemented as an actual minigame inside the game.

Monthly downloads stabilised around 4M and the title passed the $10M monthly revenues milestone for the first time in its 5th year. With this strategy, Top Games was the only Western publisher that managed to break into the Top 20 Grossing list.

So what are our predictions for 4X sub-genre in 2021?

FunPlus will hold to its lead with Lilith breathing down its neck

It’s going to be tight, but we predict that FunPlus will keep on to its sub-genre leadership while Lilith scales up Warpath during Q1. Without the IDFA depreciation, we could see Lilith coming out on top at the end of 2021.

Innovation in core gameplay will become mandatory for new titles

Top War blazed a new trail in 4X and proved that simplified core and casual mechanics can work in 4X subgenre.

IDFA depreciation will significantly slow down the scaling up of 4X titles

IDFA changes will change the UA landscape of the 4X market and make UA more difficult where usually 4X games rely on heavy targeting of high-value users and operating with low DAU/high LTV models.

4X will go cross-platform

Much like with mobile RPGs to battle the IDFA depreciation we’ll see top 4X titles offering downloadable PC clients

IP? Yes, please!

Western publishers have shown that the way to succeed against their Chinese rivals is by employing a fitting IP. We expect at least Avatar to break into the Top 20 in 2022. And then there’s the Star Wars game being cooked at EA (based on the job ads).

Wild card: We’ll see attempts at a more accessible 4X game. Think of Settlers. Or Clash of Clans. But with a persistent map populated with real players. With IDFA depreciation, wide appeal and wider monetization will likely work better than the current whale hunting model.